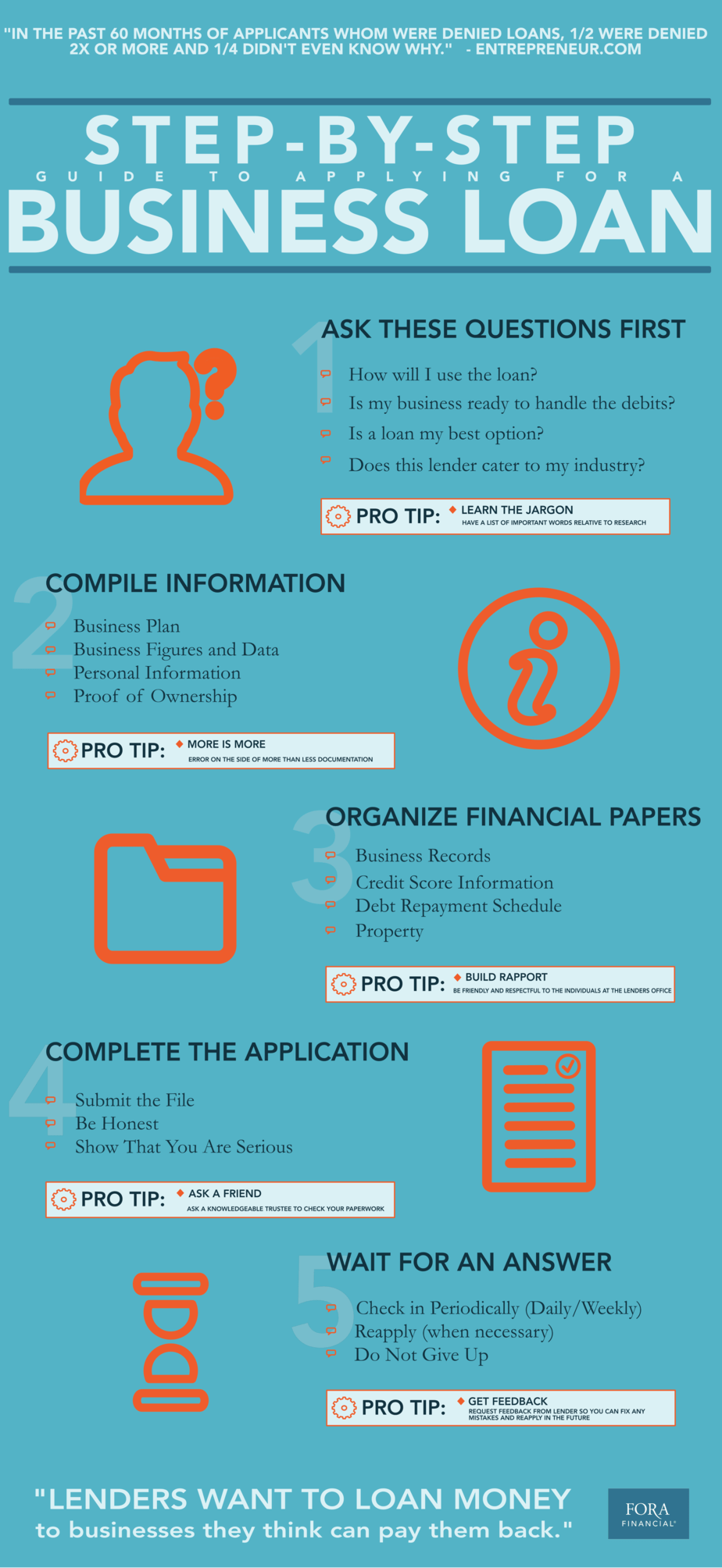

How to Get a Small Business Loan: A Comprehensive Guide

Small businesses are the backbone of our economy, but accessing capital can be a daunting task. If you’re looking to finance your small business, securing a loan can be a smart move. But before you dive into the application process, it’s crucial to understand the steps involved and the factors that will influence your success. We will break down how to get a small business loan, from determining your needs to closing the deal.

2. Prepare Your Application

Once you know what type of loan you need and where to apply, it’s time to prepare a strong application. This is your chance to make a compelling case for your business and convince the lender that you’re a good risk. Your application should include:

- A detailed business plan outlining your company’s goals, strategies, and financial projections.

- Financial statements showing your business’s income, expenses, and assets.

- Personal financial statements if you’re applying for a loan that requires a personal guarantee.

- A list of collateral, if any, that you can offer to secure the loan.

- A strong credit score and history.

Be prepared to answer questions about your business, your financial situation, and your plans for the future. The more information you can provide, the better your chances of being approved for a loan.

Expert Tip: Don’t apply for too many loans at once. Each application will result in a hard credit inquiry, which can lower your credit score. If you’re denied a loan, wait a few months before applying again.

How to Secure a Small Business Loan: A Comprehensive Guide

1. Determine Your Financing Needs

Before embarking on the loan application process, it’s crucial to have a clear understanding of your funding requirements. Ask yourself: How much capital is needed to jumpstart or expand your small business? What are the specific purposes for which the funds will be used? This self-assessment will guide your search for the most suitable financing options aligning with your business objectives.

2. Explore Funding Options

The small business loan landscape is vast, offering a myriad of lending products tailored to different needs. Term loans provide a lump sum repayment over a fixed duration, while lines of credit resemble revolving credit cards, allowing you to borrow and repay funds as needed. SBA-backed loans, offered through the Small Business Administration, come with favorable terms and reduced risk for lenders. Research these options thoroughly to determine the best fit for your situation.

3. Prepare a Strong Loan Application

A well-prepared loan application is the cornerstone of a successful funding request. Lenders will meticulously evaluate your business plan, financial statements, and personal credit history. Ensure your business plan is comprehensive, outlining your business concept, market analysis, and financial projections. Your financial statements should accurately reflect your business’s health and financial stability. Lastly, work towards improving your personal credit score, as it heavily influences your loan approval chances.

4. Shop Around for the Best Rates

Don’t settle for the first loan offer that comes your way. Take the time to compare rates, terms, and fees from multiple lenders. Consider online lenders alongside traditional banks and credit unions. By shopping around, you’ll increase your chances of securing the most favorable loan terms that match your specific business needs.

5. Be Prepared to Provide Collateral

In many cases, lenders require collateral to secure the loan. This could be personal or business assets such as real estate, inventory, or equipment. Providing collateral can significantly improve your chances of loan approval and potentially lower your interest rates. However, it’s important to weigh the risks and benefits of putting up collateral against the potential benefits of the loan.

6. Underwriting and Approval: Unlocking the Gate to Funding

Once you’ve meticulously crafted your business plan and tirelessly gathered supporting documents, the final hurdle awaits: underwriting and approval. This crucial stage is like a gatekeeper, determining whether your small business loan application will see the light of day. The lender will don the hat of an investigator, examining every nook and cranny of your application, assessing your creditworthiness, and ultimately making a decision that will shape the future of your business.

Factors Influencing the Decision

The underwriting process is not a whimsical exercise; it’s a methodical evaluation of your business’s financial health and prospects. Lenders will scrutinize your credit score, cash flow, and debt-to-income ratio, searching for indicators of your ability to repay the loan. They’ll also take a microscope to your business plan, evaluating its soundness, market potential, and projected profitability.

The Art of Persuasion: Crafting a Compelling Case

Just as a lawyer presents a persuasive case in court, you must craft a compelling business plan that convinces the lender of your venture’s viability. Highlight your unique value proposition, demonstrate a thorough understanding of your target market, and provide realistic financial projections. Remember, the lender is not simply a money-dispensing machine; they’re investing in your business, and they want to see a solid plan that inspires confidence.

Collateral and Personal Guarantees: Adding Weight to Your Loan

In some cases, lenders may request collateral to secure the loan. This could be in the form of real estate, equipment, or inventory. By pledging collateral, you’re essentially putting your assets on the line, which can increase your chances of approval. Additionally, personal guarantees may be required, where you pledge your personal assets as backing for the loan.

The Wait is Over: Receiving the Verdict

After a thorough review, the lender will deliver their verdict. If you’ve successfully navigated the underwriting process, congratulations! You’ve earned the green light for funding. If, however, your application falls short, don’t be disheartened. Seek feedback from the lender to identify areas for improvement and strengthen your application for the future. The path to small business loan approval can be challenging, but with careful preparation and a compelling case, you can increase your chances of securing the funding your business needs to thrive.