The Not-So-Average Cost of Small Business Insurance

The average cost of small business insurance varies widely depending on several factors, including the industry, location, number of employees, and coverage limits. However, according to the Insurance Information Institute, small businesses can expect to pay anywhere from $500 to $5,000 per year for general liability insurance, the most common type of business insurance.

The Importance of Small Business Insurance

Small business insurance is crucial for protecting your business from financial losses due to unexpected events. It provides peace of mind and ensures your business’s continuity. Without insurance, a single lawsuit or disaster could bankrupt your business. Think of it as a financial parachute, protecting you from the unexpected twists and turns of running a business. Just like a seatbelt in a car, it’s not something you hope to use, but it’s there to keep you safe when you need it most.

Business insurance policies typically cover a range of risks, including property damage, liability, and business interruption. They can also provide coverage for specific needs, such as cyber liability or errors and omissions insurance. Choosing the right coverage for your business is essential, as it can help you avoid financial ruin in the event of a covered loss. Without the right coverage, a minor fender bender could turn into a major headache for your business.

Small business insurance is not just a smart financial move; it’s often a legal requirement. Many states require businesses to carry certain types of insurance, such as workers’ compensation insurance. Failure to comply can result in fines or even legal action. So, before you open your doors for business, make sure you have the proper insurance coverage in place. It’s like building a house – you need a solid foundation to keep everything standing strong.

Average Cost of Small Business Insurance

The average cost of small business insurance can vary widely depending on a number of factors, including the industry you’re in, the size of your business, where you’re located, and the level of coverage you need. But as a general rule of thumb, small businesses can expect to pay between $500 and $2,000 per year for basic coverage. That’s like paying for a couple extra cups of coffee a month.

If you’re just starting out, you may be wondering if you really need business insurance. After all, you’re just a small business. But even small businesses can face big risks, like property damage, lawsuits, and employee injuries. And without insurance, you could be on the hook for these costs out of your own pocket.

So, how much does small business insurance cost? It depends on a number of factors, including:

Types of Coverage

The type of coverage you need will play a big role in the cost of your insurance. Some of the most common types of coverage for small businesses include:

General liability insurance:

This type of insurance protects your business from claims of bodily injury or property damage caused by your products, services, or operations. It’s a must-have for any small business.

Property insurance:

This type of insurance protects your business’s physical assets, such as your building, equipment, and inventory. It’s important to have enough property insurance to cover the full value of your assets.

Business interruption insurance:

This type of insurance protects your business from lost income if you have to suspend operations due to a covered event, such as a fire or natural disaster.

Workers’ compensation insurance:

This type of insurance provides benefits to employees who are injured or become ill on the job. It’s required by law in most states.

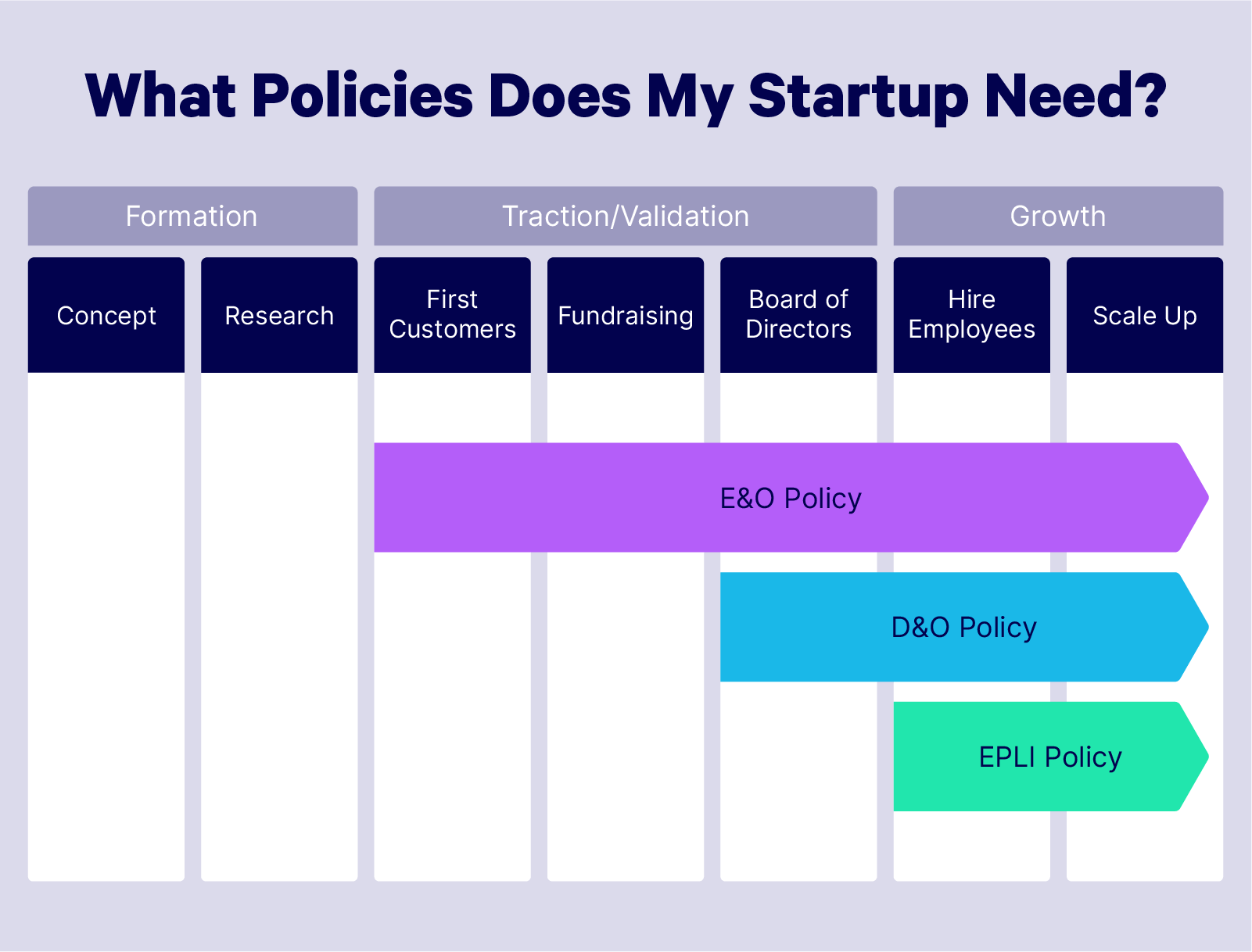

Depending on your industry and the risks that you face, you may also need additional types of coverage, such as professional liability insurance, cyber liability insurance, or product liability insurance.

Average Cost of Small Business Insurance: What You Need to Know

Navigating the world of small business insurance can be a bit like herding cats – confusing and overwhelming. But, just like wrangling those feisty felines, understanding the average cost of small business insurance can help you get a handle on the situation. According to recent industry data, the average annual premium for small business insurance hovers around $750, but this number can vary significantly depending on a few key factors. Like a chameleon blending into its surroundings, your insurance costs will adapt based on the unique characteristics of your business. Let’s dive into the factors that can affect your insurance premiums, so you can make informed decisions and keep your business purring like a well-oiled machine.

Types of Coverage: Not All Policies Are Created Equal

When it comes to small business insurance, there’s no one-size-fits-all solution. The type of coverage you choose will have a big impact on your premium. Think of it like a buffet – you can’t expect to pay the same price for a plate piled high with lobster and caviar as you would for a few slices of pizza. Similarly, a comprehensive policy that covers a wide range of risks will cost more than a basic policy that only provides essential protection. It’s like choosing between a Swiss Army knife and a butter knife – they both have their uses, but one is clearly more versatile and comes with a heftier price tag.

Policy Limits: Dialing Up the Coverage, Dialing Up the Cost

Policy limits are like the speed limit for your insurance coverage. The higher the limits, the more your insurance will pay out in the event of a covered claim. But, just like exceeding the speed limit can result in a hefty fine, increasing your policy limits will also increase your premium. It’s a delicate balancing act – you want enough coverage to protect your business from financial ruin, but you don’t want to overpay for coverage you may never need. Think of it like buying a car – you could opt for a compact car that gets great gas mileage, or you could splurge on a luxury SUV with all the bells and whistles. Both will get you from point A to point B, but the price difference is significant.

Deductibles: The Trade-Off Between Risk and Reward

A deductible is the amount you have to pay out of pocket before your insurance coverage kicks in. It’s like a financial buffer that you agree to absorb in exchange for a lower premium. The higher the deductible, the lower your premium will be. But, if you have a high deductible, you’ll have to pay more out of pocket if you need to file a claim. It’s a bit like playing a game of chicken – you’re willing to take on more risk (higher deductible) in the hopes of avoiding a major financial hit (lower premium). Just be sure you’re prepared to pay the deductible if you need to make a claim.

**Navigating the Maze of Small Business Insurance Costs**

The average cost of small business insurance is like a well-kept secret, leaving many entrepreneurs in the dark. But fret not! We’re here to shed light on this enigmatic expense, breaking it down into digestible chunks. So, buckle up and prepare to demystify the world of business insurance premiums.

**Breakdown of Insurance Premiums**

Just like a complex financial puzzle, small business insurance premiums are an intricate tapestry of various costs. Here are the key components to keep in mind:

**Base Policy Costs:**

This is the foundation of your insurance coverage, like the bedrock of a sturdy building. It provides you with essential protection against common risks like property damage, liability claims, and business interruption.

**Coverage Riders:**

Think of these as add-ons to your base policy, like toppings on a pizza. They extend your coverage to specific areas that your base policy might not cover, such as cyber liability, employee dishonesty, or extra property coverage.

**Taxes and Fees:**

Just like the IRS doesn’t miss a beat, you’ll also need to factor in taxes and fees that may apply to your insurance premium. These might include state premium taxes or fees imposed by your insurance carrier.

**Factors Influencing Premiums**

Now, let’s dive deeper into the factors that can dance around your insurance premiums like nimble acrobats:

**Insurance Coverage Limits:**

Higher coverage limits are like an invisible force field for your business, but they come at a higher cost. Similarly, lower coverage limits will set you back less, but they might leave your business vulnerable in certain scenarios.

**Business Location:**

Like a weather vane that predicts the direction of the wind, the location of your business can also shape your insurance premiums. Areas with higher risks, such as those prone to natural disasters or crime, typically command higher premiums.

**Industry Type:**

Different industries carry varying levels of risk, and this risk appetite translates directly into insurance costs. For instance, businesses that work with heavy machinery might face higher premiums compared to those that primarily deal with paperwork.

**Claims History:**

Your claims history is like a report card that insurance companies scrutinize. A clean claims record can earn you premium discounts, while a history of frequent claims might result in higher premiums.

Average Cost of Small Business Insurance

The average cost of small business insurance in the United States is around $2,000 per year, according to the Insurance Information Institute. Small businesses account for a large portion of the U.S. economy, and they face unique risks that can be mitigated by insurance. This article will explore the average cost of small business insurance and provide tips on how to save money on your premiums.

Factors Affecting the Cost of Insurance

The cost of small business insurance varies depending on several factors, including the size, industry, location, and number of employees of the business. Other factors that can affect the cost of insurance include the coverage limits and deductibles chosen by the business. Insurers use these factors to calculate the risk of insuring a business and set premiums accordingly.

Bundling Insurance Policies

One way to save money on small business insurance is by bundling insurance policies. Businesses can bundle their property, liability, and workers’ compensation insurance into a single policy, which can result in lower premiums than purchasing each policy separately. Bundling insurance policies is a good option for businesses that need multiple types of coverage.

Increasing Deductibles

Another way to lower small business insurance costs is by increasing deductibles, which is the amount that the business pays out of pocket before the insurance company begins to cover claims. By increasing deductibles, businesses can lower their premiums, but they should be aware that they will have to pay more out of pocket in the event of a claim. Businesses should carefully consider their financial situation and risk tolerance before increasing deductibles.

Implementing Loss Control Measures

One way to reduce the cost of small business insurance is by implementing loss control measures, which are measures designed to prevent or reduce losses. These measures can include installing security systems, implementing safety protocols, and providing employee training. By implementing loss control measures, businesses can reduce the likelihood of claims, which can lead to lower insurance premiums. Additionally, some insurance companies offer discounts to businesses that implement loss control measures.

Tips for Saving Money on Insurance

In addition to the strategies discussed above, there are several other tips that small businesses can use to save money on insurance. These tips include:

- Shop around for insurance quotes from multiple insurers.

- Negotiate with insurance companies for lower premiums.

- Take advantage of discounts for early payment and bundling policies.

- Maintain a good claims history.

- Increase deductibles on policies that are less likely to be used, such as comprehensive auto insurance.

By following these tips, small businesses can reduce their insurance costs and protect their financial well-being.

Average Cost of Small Business Insurance

The average cost of small business insurance varies depending on a multitude of factors, but typically falls between $500 to $2,000 per year. This range covers essential coverages like general liability, property, and business interruption insurance. The actual cost for your business will depend on factors such as industry, location, number of employees, and claims history.

Factors Affecting Insurance Premiums

Several factors influence the cost of small business insurance premiums. These include:

Types of Small Business Insurance

Small businesses typically need a combination of insurance policies to protect against common risks. Here are some of the most common types:

Benefits of Small Business Insurance

Small business insurance offers numerous benefits, including:

Conclusion

Small business insurance is an essential investment that provides financial protection and peace of mind. Understanding the average cost and factors affecting insurance premiums empowers small businesses to make informed decisions about their coverage needs and budget accordingly. By carefully considering their risk exposure and choosing the right insurance policies, small businesses can protect themselves against financial setbacks and ensure their continued success.