Business Health Insurance for Small Businesses

In today’s competitive business landscape, offering comprehensive employee benefits, including health insurance, has become a strategic imperative for small businesses. Without it, how can you hope to attract and retain the best talent, boost employee morale, and drive productivity? Health insurance, in particular, plays a pivotal role in securing a healthy workforce, minimizing absenteeism, and creating a positive work environment. But how does business health insurance for small firms stack up?

Benefits of Offering Health Insurance to Employees

Investing in employee health insurance doesn’t just benefit your employees; it also pays dividends for your business. Here’s why:

Attracting and Retaining Top Talent: In a tight labor market, offering health insurance can give your small business a competitive edge when it comes to recruiting and retaining top performers. Employees are more likely to be drawn to companies that prioritize their well-being.

Increased Employee Satisfaction: When employees feel valued and taken care of, their job satisfaction skyrockets. Access to affordable health insurance is a clear demonstration of your commitment to their health and happiness.

Improved Productivity: Healthy employees are more productive employees. By providing health insurance, you’re not only helping to prevent illnesses and injuries but also reducing absenteeism, leading to a more efficient and productive workforce.

Reduced Turnover Costs: High employee turnover can be a costly headache for small businesses. Offering health insurance can help reduce turnover rates, as employees are less likely to leave a company that provides such a valuable benefit.

Improved Employee Health: Access to affordable health insurance encourages employees to seek preventive care and manage chronic conditions, leading to better overall health and a healthier workforce.

Business Health Insurance for the Little Guy

Navigating business health insurance can feel like trying to decode a foreign language. But fear not! We’re here to break it down for you, starting with the big question:

Types of Health Insurance Plans for Small Businesses

There are three main types of health insurance plans tailored for small businesses:

**1. Group Health Plans:**

These plans pool together employees’ premiums to negotiate lower rates with insurance carriers. If your business has 50 or more employees, you’re legally required to offer group health insurance.

**2. Individual Health Insurance:**

This option allows employees to purchase their own individual policies. While it offers flexibility, it typically comes with higher premiums and fewer coverage options.

**3. Health Savings Accounts (HSAs):**

HSAs are savings accounts designed to cover qualified medical expenses. They’re paired with a high-deductible health plan and offer tax advantages such as tax-free contributions, earnings, and qualified withdrawals.

HSAs: A Deeper Dive

HSAs come with a triple tax bonus! Contributions are made pre-tax, earnings grow tax-free, and qualified withdrawals are tax-free. It’s like a piggy bank for your medical needs that never runs out of bacon. Plus, HSAs give you the freedom to choose the healthcare providers that fit your needs, like a kid in a candy store with no chaperone.

So, which plan is right for your small business? Consider your budget, the number of employees, and their health needs. Remember, finding the perfect plan is like finding the lost remote – it takes some searching, but when you do, it’s a sweet victory.

Business Health Insurance for Small Businesses: A Comprehensive Guide

Health insurance is a crucial component for any small business looking to provide comprehensive benefits to its employees. However, navigating the complexities of health insurance can be daunting for small businesses. This guide aims to provide a deeper understanding of health insurance costs, plan options, and essential tips to help small businesses make informed decisions about their health insurance coverage.

Understanding Health Insurance Costs

The cost of health insurance for small businesses can vary significantly depending on several factors, including the:

- Size of the business: Premiums tend to be lower for businesses with a smaller number of employees.

- Number of employees: The more employees a business has, the higher the overall cost of health insurance.

- Geographic location: Health insurance costs can vary depending on the state or region where the business is located.

li>Type of plan chosen: Different types of health insurance plans have varying costs, with more comprehensive plans typically costing more.

To get an accurate estimate of health insurance costs, it’s essential for small businesses to consult with multiple insurance providers and compare their quotes.

Plan Options for Small Businesses

Small businesses have various health insurance plan options to choose from, each with its advantages and disadvantages. The most common types of plans include:

1.

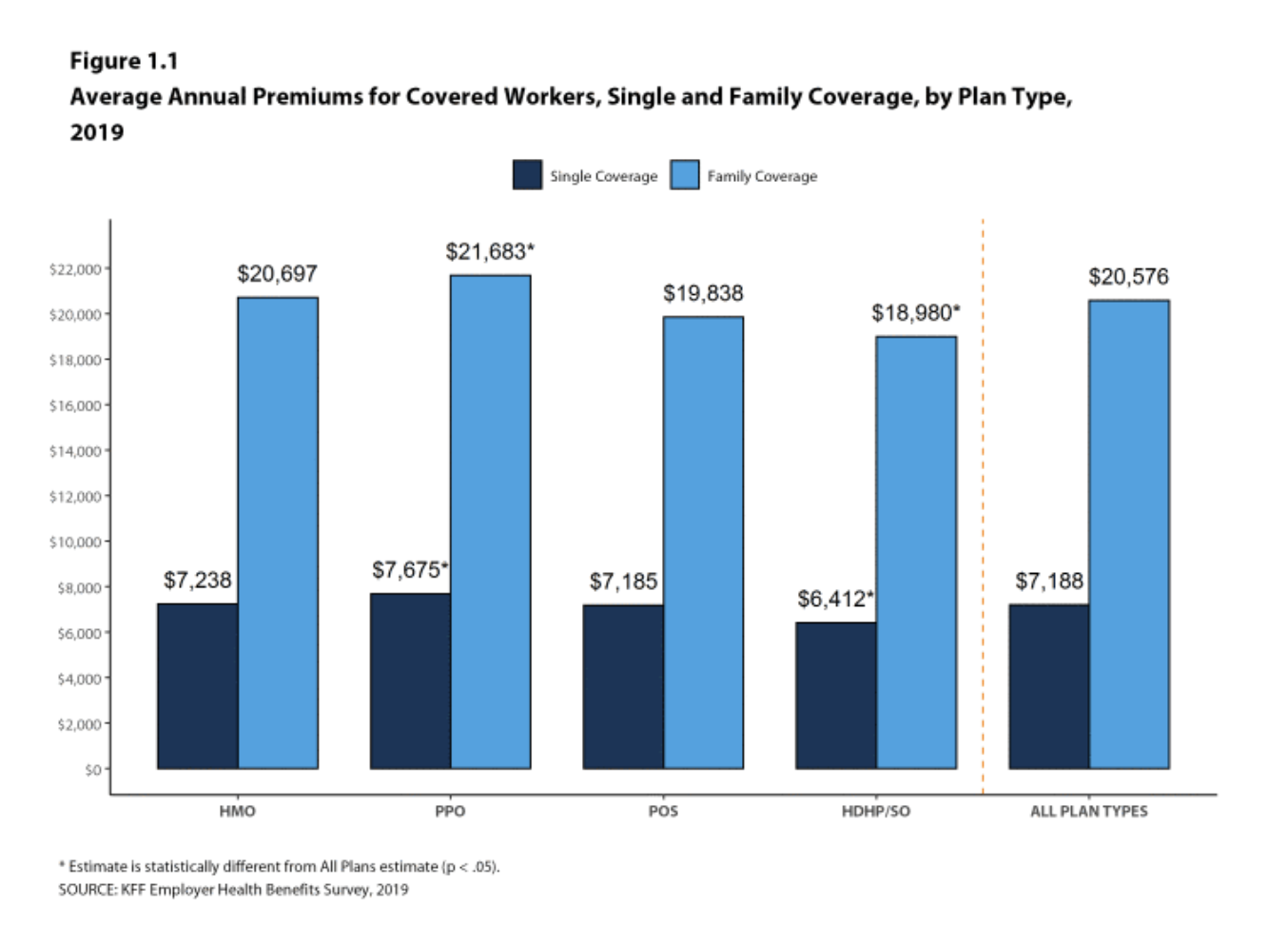

Preferred Provider Organizations (PPOs):

These plans offer flexibility in choosing healthcare providers, but they typically have higher premiums than other types of plans.

2.

Health Maintenance Organizations (HMOs):

These plans require members to use a network of providers and have lower monthly premiums than PPOs.

3.

Point-of-Service (POS) Plans:

POS plans combine features of both PPOs and HMOs, allowing members to choose providers outside of the network for a higher cost.

4.

Consumer-Directed Health Plans (CDHPs):

These plans pair a high-deductible health plan with a tax-advantaged savings account that can be used to pay for healthcare costs.

When selecting a health insurance plan, it’s essential for small businesses to consider their budget, the specific needs of their employees, and the level of flexibility and choice they desire.

Health Insurance for Small Businesses: A Comprehensive Guide

Health insurance is becoming increasingly essential for businesses of all sizes, but it can be especially daunting for small businesses with limited resources. From understanding government assistance programs to exploring private insurance options, this guide aims to provide small business owners with the information they need to make informed decisions about health coverage.

What is Business Health Insurance?

Business health insurance is a type of health insurance that covers the health-related expenses of employees and their families. It can cover a wide range of services, including preventive care, hospitalization, and prescription drugs. Health insurance provides employees with peace of mind and financial protection in the event of an illness or injury.

Government Assistance Programs for Small Businesses

Small businesses may be eligible for government assistance programs that can help them offset the cost of health insurance premiums. Here are a few programs to consider:

- The Small Business Health Options Program (SHOP): This program provides tax credits and subsidies to eligible small businesses to help them purchase health insurance for their employees.

- The Health Insurance Marketplace: This online marketplace allows small businesses to compare and purchase health insurance plans from private insurers.

- The Medicaid Expansion Program: This program extends Medicaid coverage to low-income individuals, including employees of small businesses.

Choosing a Private Insurance Plan

If you don’t qualify for government assistance, you can purchase private health insurance for your employees. When choosing a plan, consider the following factors:

- Coverage: Make sure the plan covers the services your employees need.

- Premiums: Compare the monthly premiums of different plans to find the best fit for your budget.

- Deductibles: The deductible is the amount you must pay before the insurance starts covering costs. Choose a deductible that is affordable for your employees.

- Prescription Drug Coverage: If your employees take prescription drugs, make sure the plan covers the medications they need.

Premiums and Benefits

The cost of health insurance premiums can vary widely depending on the size of your business, the number of employees, and the type of plan you choose. In general, larger businesses with more employees pay lower premiums per employee. The benefits of health insurance can outweigh the costs by improving employee morale, attracting and retaining top talent, and reducing the risk of unexpected medical expenses.

Conclusion

Health insurance is an important part of running a small business. By understanding government assistance programs, exploring private insurance options, and carefully considering your business’s needs, you can find the right health insurance plan for your employees and protect both your business and your employees’ health.