**401(k) Setup for Small Businesses: A Comprehensive Guide**

As a small business owner, you’re always looking for ways to improve your bottom line and attract top talent. Offering a 401(k) plan can be a smart move on both fronts.

**Why a 401(k) Plan?**

* **Attract and retain employees:** A 401(k) plan can be a valuable perk for employees, making your business more attractive to potential hires.

* **Reduce expenses:** Contributions to a 401(k) plan are tax-deductible, which can reduce your business’s tax liability.

* **Simplify retirement planning:** Offering a 401(k) plan can help employees save for retirement, which can take the pressure off your business in the long run.

**Types of 401(k) Plans**

There are two main types of 401(k) plans:

* **Traditional 401(k) plans:** Contributions to a traditional 401(k) plan are made with pre-tax dollars, which means they are deducted from your employee’s paycheck before taxes are taken out. This reduces your employee’s current tax liability but means that withdrawals in retirement will be taxed as income.

* **Roth 401(k) plans:** Contributions to a Roth 401(k) plan are made with after-tax dollars, which means they are not deducted from your employee’s paycheck before taxes are taken out. This means that withdrawals in retirement will be tax-free.

**Which Type of 401(k) Plan Is Right for My Business?**

The best type of 401(k) plan for your business depends on a number of factors, including your employees’ age, income, and retirement goals. It’s a good idea to talk to a financial advisor to determine which type of plan is right for you.

**How to Set Up a 401(k) Plan**

Setting up a 401(k) plan can seem like a daunting task, but it doesn’t have to be. Here are the steps you need to take:

1. **Choose a plan provider.** There are a number of different plan providers out there, so it’s important to do your research and find one that’s right for you.

2. **Establish a plan document.** This document will outline the rules of your plan, including who is eligible to participate, how much they can contribute, and when they can withdraw their money.

3. **Open a trust account.** This account will hold the assets of your plan.

4. **Enroll your employees.** Once you have established your plan, you will need to enroll your employees.

5. **Make contributions.** You will need to make regular contributions to your plan, either on a pre-tax or after-tax basis.

**Tips for Managing Your 401(k) Plan**

Once you have set up your 401(k) plan, it’s important to manage it carefully. Here are a few tips:

* **Review your plan regularly.** Make sure that your plan is still meeting the needs of your business and your employees.

* **Make sure your employees are contributing enough.** The more your employees contribute to their 401(k) plans, the more they will have saved for retirement.

* **Get help from a financial advisor.** If you need help managing your 401(k) plan, don’t hesitate to get help from a financial advisor.

**401k Setup for Small Businesses: A Comprehensive Guide**

Small businesses play a crucial role in the economy, and their employees deserve access to retirement savings plans. Setting up a 401k plan can be a valuable benefit for employees, but it can seem daunting for small business owners. This comprehensive guide will walk you through the process, from selecting a provider to making sure your plan meets your needs.

**Selecting a Provider**

Choosing the right provider for your 401k plan is essential. Consider factors like fees, investment options, customer support, and flexibility of plan design. Compare multiple providers to find one that fits your needs and budget.

**Enrolling Employees**

Once you’ve selected a provider, it’s time to enroll your employees. Communicate the benefits of the plan and explain how it works. Make sure they understand the rules and regulations surrounding 401k plans.

**Setting Contribution Amounts**

Determine the contribution limits for your employees and the company. You have the flexibility to set different contribution levels for different employees. Consider affordability, employee needs, and your financial goals.

**Making Investments**

Your 401k plan will offer a variety of investment options. Help your employees understand the risks and returns associated with each option. Provide them with educational materials and investment advice if needed.

**Monitoring and Maintaining**

Once your 401k plan is set up, monitor it regularly to ensure it’s performing as expected. Review investment performance, make adjustments as necessary, and communicate updates to your employees. Oh, and don’t forget about the ever-changing regulatory landscape—stay up-to-date on any new rules or requirements.

Set Up a 401k for Your Small Business

Seeking methods to entice and maintain a stellar staff? Look no further than establishing a 401(k) plan for your small business. A 401(k) is not only a valuable job perk in today’s competitive employment market, but it can also offer substantial tax benefits for both your company and employees.

Setting Up the Plan

The first step in setting up a 401(k) plan is to generate a plan document that outlines the program’s regulations. Once written up, you’ll need to apply for a unique plan identification number from the Internal Revenue Service (IRS). Once approved, having a clear outline of the plan’s rules, regulations, and guidelines will be vital to ensuring its smooth operation.

Choosing a Plan Provider

Next, select a plan provider that aligns with your company’s needs. There are many providers out there, so do your research and compare features, fees, and investment options. Don’t be afraid to ask questions and read reviews to make sure you’re comfortable with your choice.

Start Contributing

Once you’ve chosen a provider, start contributing to the plan. You can choose to contribute a fixed amount each pay period, or you can set up automatic contributions. Contributions can be made by the employee, employer, or both. The limits on employee contributions are adjusted annually by the IRS, so check the current guidelines to ensure compliance.

Invest Wisely

The money in your 401(k) account can be invested in a variety of ways. You can choose a mix of stocks, bonds, and mutual funds that align with your risk tolerance and financial goals. With time and thoughtful considerations, these investments have the potential to grow and generate long-term wealth.

Communicate with Employees

Once your 401(k) plan is up and running, communicate its existence and the benefits to your employees. Make sure they understand how the plan works and how they can participate. Consider using visual aids to present information in an engaging manner. The more informed your employees are, the more likely they are to take advantage of this valuable benefit.

**401k Setup for Small Business: A Comprehensive Guide**

As a small business owner, providing a retirement plan for your employees is not just a smart financial move, it’s also a great way to attract and retain top talent. Among the various retirement plans available, 401ks stand out as a popular and effective option. Here’s a comprehensive guide to help you get started with setting up a 401k plan for your small business.

**Understanding the Basics**

A 401k plan is a tax-advantaged retirement savings account that allows employees to contribute a portion of their pre-tax income to invest for retirement. Contributions and investment earnings grow tax-free until withdrawn during retirement, when they are taxed as ordinary income. Employers can also make matching contributions to employees’ accounts, which can further enhance savings.

**

Contribution Rules

**

* **Contribution Limits:** Contribution limits vary annually and are set by the Internal Revenue Service (IRS). For 2023, the limit for employee elective deferrals is $22,500, while employers can contribute up to 100% of an employee’s compensation, up to a maximum of $66,000 (plus a catch-up contribution of $7,500 for employees age 50 and older).

* **Employee Eligibility:** Most employees are eligible to participate in a 401k plan after completing one year of service. However, employers can also use a shorter eligibility period, such as 90 days.

* **Matching Contributions:** Employers are not required to offer matching contributions, but many do as a way to encourage employee participation and save for retirement. Matching contributions can vary in structure, but the most common is a dollar-for-dollar match up to a certain percentage of an employee’s salary, such as 50% up to 6%.

**

Plan Design Options

**

* **Traditional vs. Roth 401k:** Traditional 401ks offer tax-deferred savings, meaning contributions are deducted from an employee’s pre-tax income and earnings grow tax-free until withdrawn during retirement. Roth 401ks, on the other hand, offer tax-free withdrawals in retirement, but contributions are made with after-tax dollars.

* **Safe Harbor Plans:** Safe harbor plans are a type of 401k that automatically satisfies the IRS’s non-discrimination testing requirements, which ensure that plans do not disproportionately benefit highly compensated employees. Employers must meet specific contribution requirements to qualify for safe harbor status.

**

Investment Options

**

* **Investment Menu:** Plan participants should have a range of investment options to choose from, such as mutual funds, target-date funds, and stable value funds. Employers should consider both the fees associated with each fund and the risk tolerance of their employees.

* **Default Investment Option:** For employees who do not actively choose investments, a default investment option, such as a target-date fund, should be provided. Target-date funds automatically adjust the asset allocation based on the participant’s age and retirement date, providing a balanced approach to saving.

**

Fiduciary Responsibilities

**

* **Plan Sponsors:** Employers are considered plan sponsors and have a fiduciary duty to act in the best interests of plan participants. This includes selecting plan investments, monitoring the plan’s performance, and providing participants with accurate information about the plan.

* **Investment Committee:** Employers may establish an investment committee to assist with investment selection and oversight. The investment committee can be made up of internal staff, external advisors, or a combination of both.

**

Ongoing Administration

**

* **Administration Fees:** Employers are responsible for paying ongoing administrative fees associated with the plan, such as recordkeeping and investment management. These fees can vary depending on the size and complexity of the plan.

* **Regular Reporting:** Plan sponsors must file annual reports with the IRS and provide participants with regular updates on their account balances and investment performance.

**

Conclusion

Setting up a 401k plan for your small business can be a valuable step in providing retirement security for your employees. By understanding the contribution rules, plan design options, investment options, and fiduciary responsibilities involved, you can design a plan that meets the specific needs of your business and helps your employees save for a secure financial future.

**401(k) Setup for Small Businesses: A Comprehensive Guide**

As a savvy small business owner, you’re always looking for ways to attract and retain top-notch employees. Offering a 401(k) retirement plan is a powerful tool that can give you a competitive edge in today’s market. But setting up a 401(k) can seem like a daunting task, especially if you’re new to the process. That’s where we come in. In this comprehensive guide, we’ll walk you through everything you need to know, from eligibility requirements to investment options.

**Eligibility Requirements**

The first step is to determine if you’re eligible to offer a 401(k) plan. If you employ at least one person other than yourself, you’re generally eligible. There are some exceptions, but they’re relatively rare.

**Plan Selection**

Once you’ve determined that you’re eligible, the next step is to choose a plan. There are two main types of 401(k) plans: traditional and Roth. Traditional plans offer tax-deferred growth, meaning you don’t pay taxes on your contributions until you withdraw them in retirement. Roth plans offer tax-free growth, meaning you don’t pay taxes on your withdrawals in retirement, but you pay taxes on your contributions upfront.

**Employee Education**

Once you’ve chosen a plan, it’s important to educate your employees about it. This includes providing clear and accessible information about the plan, its benefits, and investment options. You should also encourage employees to participate in the plan, and you may even consider offering matching contributions to sweeten the pot.

**Investment Options**

Most 401(k) plans offer a variety of investment options, including stocks, bonds, and mutual funds. It’s important to choose investment options that meet the needs of your employees. If you’re not sure what investment options are right for you, you can consult with a financial advisor.

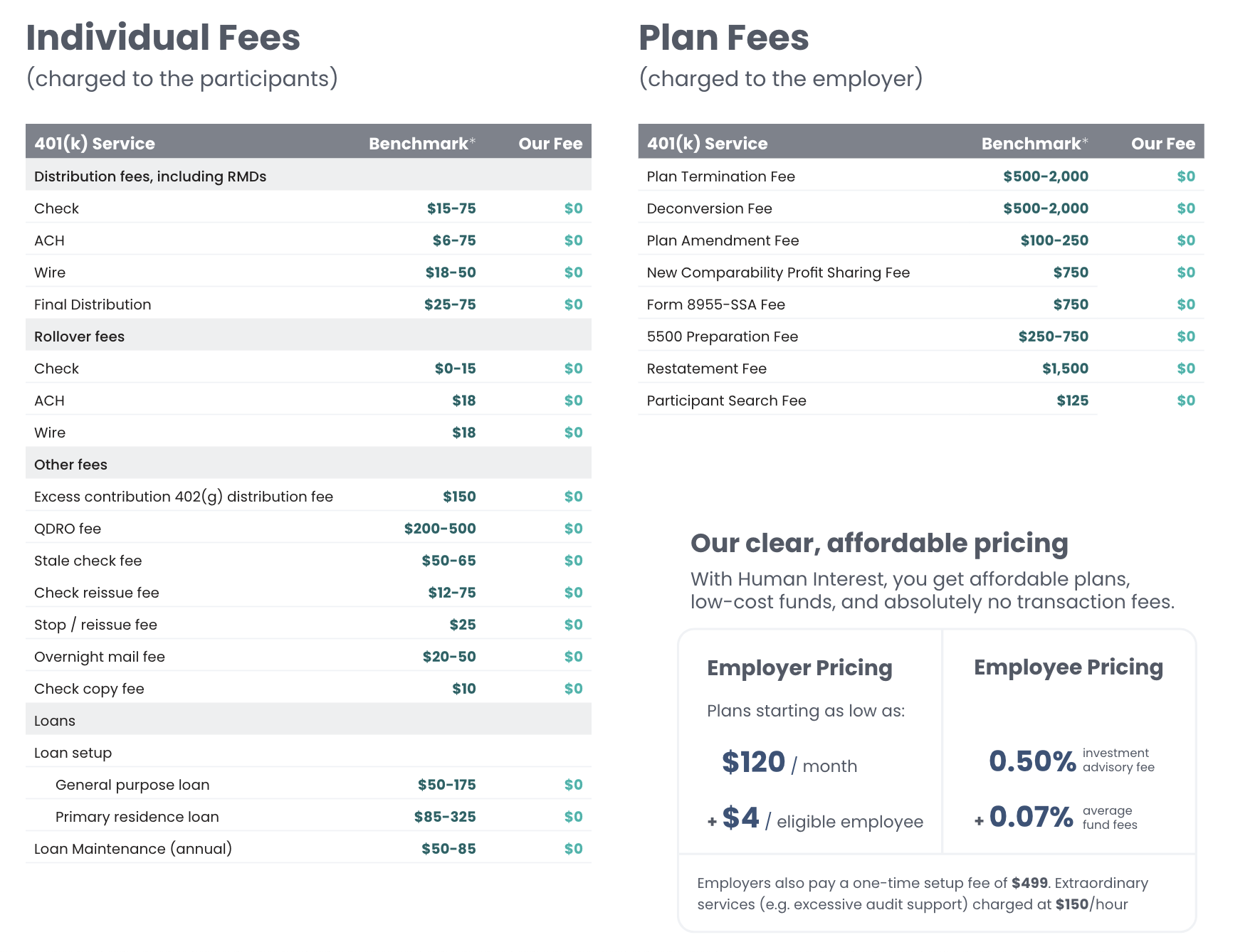

**Fees**

There are a variety of fees associated with 401(k) plans, including administrative fees, investment management fees, and withdrawal fees. It’s important to understand these fees before you choose a plan. You should also shop around for plans to find the one with the lowest fees.

**Contribution Limits**

The amount of money that you and your employees can contribute to a 401(k) plan is limited by law. For 2023, the contribution limit is $22,500. If you’re over the age of 50, you can make catch-up contributions of up to $7,500.

**Vesting**

Vesting refers to the process of employees gaining ownership of their 401(k) contributions. Once you’re vested, your contributions are yours to keep, even if you leave your job. Vesting typically occurs over a period of time, such as 3 or 5 years.

**Taxes**

401(k) plans are subject to a variety of taxes, including income taxes, capital gains taxes, and estate taxes. It’s important to understand these taxes before you contribute to a 401(k) plan. You should also consult with a tax advisor to learn how your 401(k) contributions will affect your taxes.